Three Portfolios, Three Risk Levels, Real-World Results

One of the most common questions investors ask is simple:

"What is the best portfolio?"

The answer is surprisingly unsatisfying.

There is no universally best portfolio.

The best portfolio is the one that aligns with your goals, time horizon, financial situation, and ability to stay invested during difficult periods.

Many investors focus almost exclusively on returns. They want to know which portfolio produced the highest gains over time.

While returns certainly matter, they are only part of the story.

Every increase in expected return typically comes with a tradeoff. Higher returns generally require accepting higher volatility, larger declines during market crashes, and longer recovery periods.

The chart above compares three diversified portfolios with different levels of risk and reward.

Each portfolio uses the same basic building blocks:

- U.S. Stocks

- International Stocks

- Intermediate-Term Bonds

- Short-Term Bonds

The difference is how those assets are combined.

Understanding these tradeoffs can help investors build portfolios they can stick with through both good times and bad.

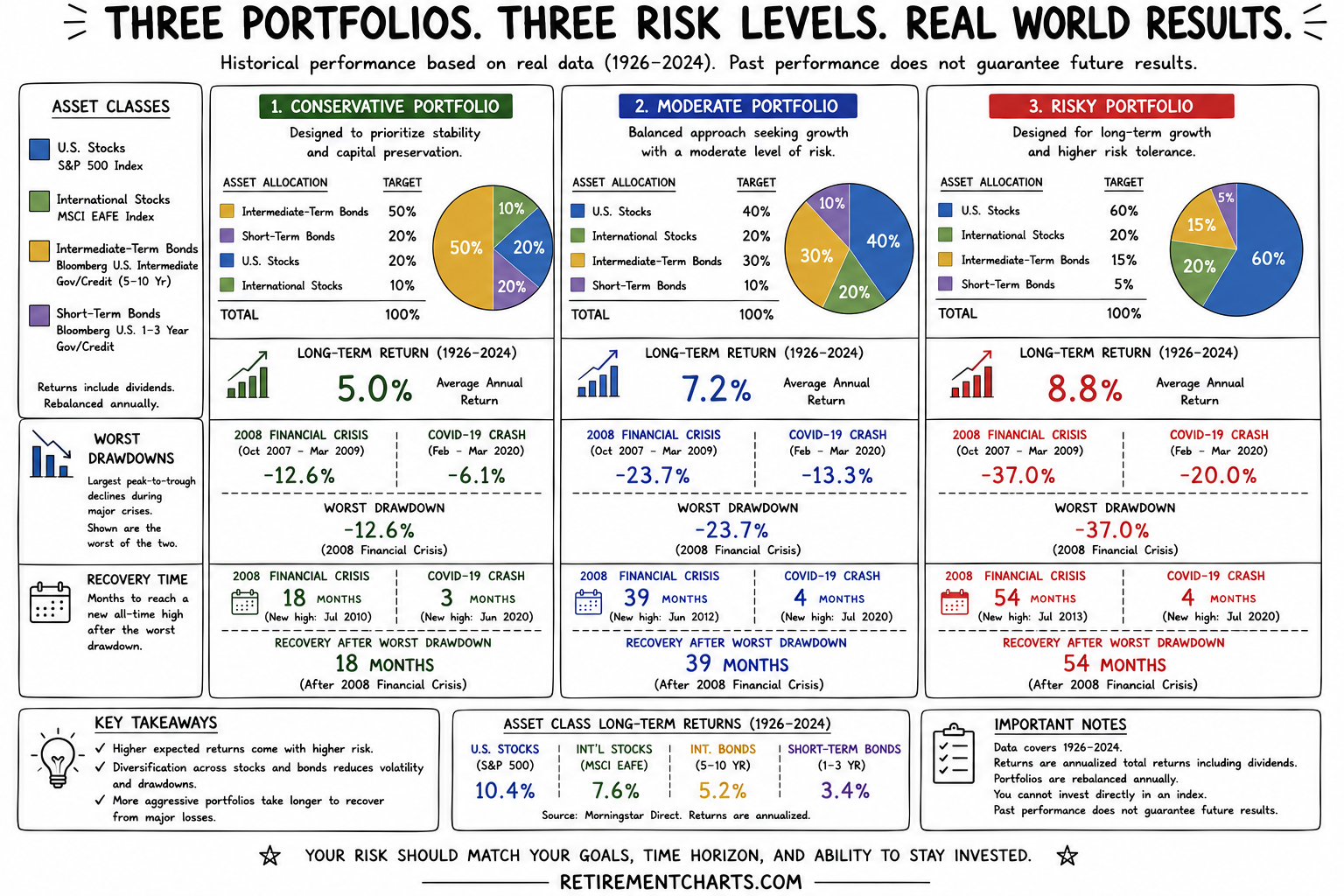

The Conservative Portfolio

The conservative portfolio is designed for stability and capital preservation.

This portfolio allocates approximately 70% to bonds and 30% to stocks.

The goal is not to maximize returns. The goal is to reduce volatility and provide a smoother investment experience.

Historically, this type of portfolio has produced annual returns around 5%.

That return may not sound exciting compared to stock-heavy portfolios, but it comes with a meaningful benefit: significantly smaller declines during major market downturns.

During the 2008 Financial Crisis, a conservative portfolio experienced a drawdown of roughly 12%.

While no investor enjoys losses, a decline of that size is generally much easier to tolerate than a decline approaching 40% or 50%.

The recovery period was also relatively short.

Because the decline was smaller, the portfolio was able to recover more quickly and return to new highs sooner.

For retirees, near-retirees, or investors with lower risk tolerance, this stability can be extremely valuable.

The downside is that lower volatility often means lower long-term growth.

A conservative portfolio may help investors sleep better at night, but it is unlikely to produce the highest wealth accumulation over several decades.

The Moderate Portfolio

The moderate portfolio represents the classic balanced approach.

This portfolio maintains approximately a 60/40 stock-to-bond allocation.

Historically, versions of the 60/40 portfolio have served as the foundation for many retirement plans and investment strategies.

The appeal is straightforward.

Investors receive meaningful exposure to stock market growth while still benefiting from the stabilizing influence of bonds.

Historically, balanced portfolios have generated annual returns around 7%.

While that difference may seem small compared to the conservative portfolio, the impact compounds significantly over time.

An additional 2% per year may not sound dramatic, but over twenty or thirty years it can result in substantially larger account balances.

The tradeoff is greater volatility.

During the Financial Crisis of 2008, moderate portfolios experienced losses in the neighborhood of 20% to 25%.

Those declines are larger than conservative portfolios but significantly smaller than stock-heavy portfolios.

Recovery periods also tend to be longer.

Investors must remain patient and disciplined while waiting for markets to recover.

For many individuals, the moderate portfolio represents a practical middle ground.

It seeks growth while still recognizing that most investors need some level of downside protection.

The Risky Portfolio

The risky portfolio is designed primarily for long-term growth.

This portfolio allocates roughly 80% to stocks and 20% to bonds.

Historically, portfolios with this structure have generated annual returns approaching 9%.

Over long periods, that additional growth can be powerful.

Higher stock allocations allow investors to participate more fully in economic growth, rising corporate earnings, and long-term market appreciation.

However, those higher returns come at a cost.

During severe bear markets, stock-heavy portfolios can experience substantial declines.

The Financial Crisis provides an excellent example.

Portfolios with approximately 80% stock exposure experienced losses approaching 40%.

For many investors, those declines feel very different in practice than they appear on paper.

It is easy to say you can tolerate a 40% decline when markets are rising.

It becomes much more difficult when the decline is actually occurring and headlines suggest things may get worse.

The recovery period is also longer.

After a major drawdown, aggressive portfolios often require several years before reaching new highs.

This is one of the most overlooked aspects of risk.

Most investors focus on how much a portfolio can lose.

Few focus on how long they may need to wait to fully recover.

The ability to remain invested during those periods is often what separates successful investors from unsuccessful ones.

The Real Risk Is Behavioral

Many investors believe risk is measured solely by volatility.

In reality, behavioral risk may be even more important.

A portfolio only works if you can stick with it.

An aggressive portfolio may produce higher expected returns, but those returns are meaningless if an investor panics during a bear market and sells at the worst possible time.

Likewise, an overly conservative portfolio may feel comfortable, but it may not provide enough growth to support future retirement spending.

The challenge is finding the balance between risk and comfort.

The ideal portfolio is not the one with the highest return.

It is the one that allows you to remain disciplined through all market environments.

Investors often overestimate their risk tolerance during bull markets and underestimate it during bear markets.

This is why understanding historical drawdowns can be so valuable.

The numbers provide context before the next crisis arrives.

Diversification Matters

Another lesson from the chart is the importance of diversification.

None of these portfolios relies entirely on a single asset class.

Each combines multiple investments with different characteristics.

Stocks provide growth.

Bonds provide stability.

International investments provide additional diversification.

Short-term bonds help reduce volatility.

Together, these components create portfolios that are more resilient than any individual asset class on its own.

Diversification does not eliminate risk.

It does, however, help manage risk in a way that can improve the overall investing experience.

The Bottom Line

Every portfolio involves tradeoffs.

Higher expected returns typically require accepting larger declines and longer recovery periods.

Lower volatility often means sacrificing some long-term growth.

The goal is not to find the perfect portfolio.

The goal is to find the portfolio that best matches your goals, time horizon, and ability to stay invested.

A conservative investor who remains disciplined will often outperform an aggressive investor who continually changes strategies.

Successful investing is not about maximizing returns at all costs.

It is about building a portfolio you can stick with through both bull markets and bear markets.

Because in the end, the portfolio that works best is the one you actually keep.