The Relationship Between Time and Risk

One of the most common investing mistakes is assuming that risk is a fixed characteristic of an investment.

Many people view stocks as risky, bonds as safe, and cash as the safest option available. While there is some truth to that statement in the short term, the reality is far more nuanced.

Risk changes over time.

In fact, one of the most important concepts in investing is understanding that an asset's risk profile often depends on your investment horizon. An investment that appears risky over a few months may be considerably less risky over several decades. Likewise, an asset that appears safe today may create significant risk over longer periods.

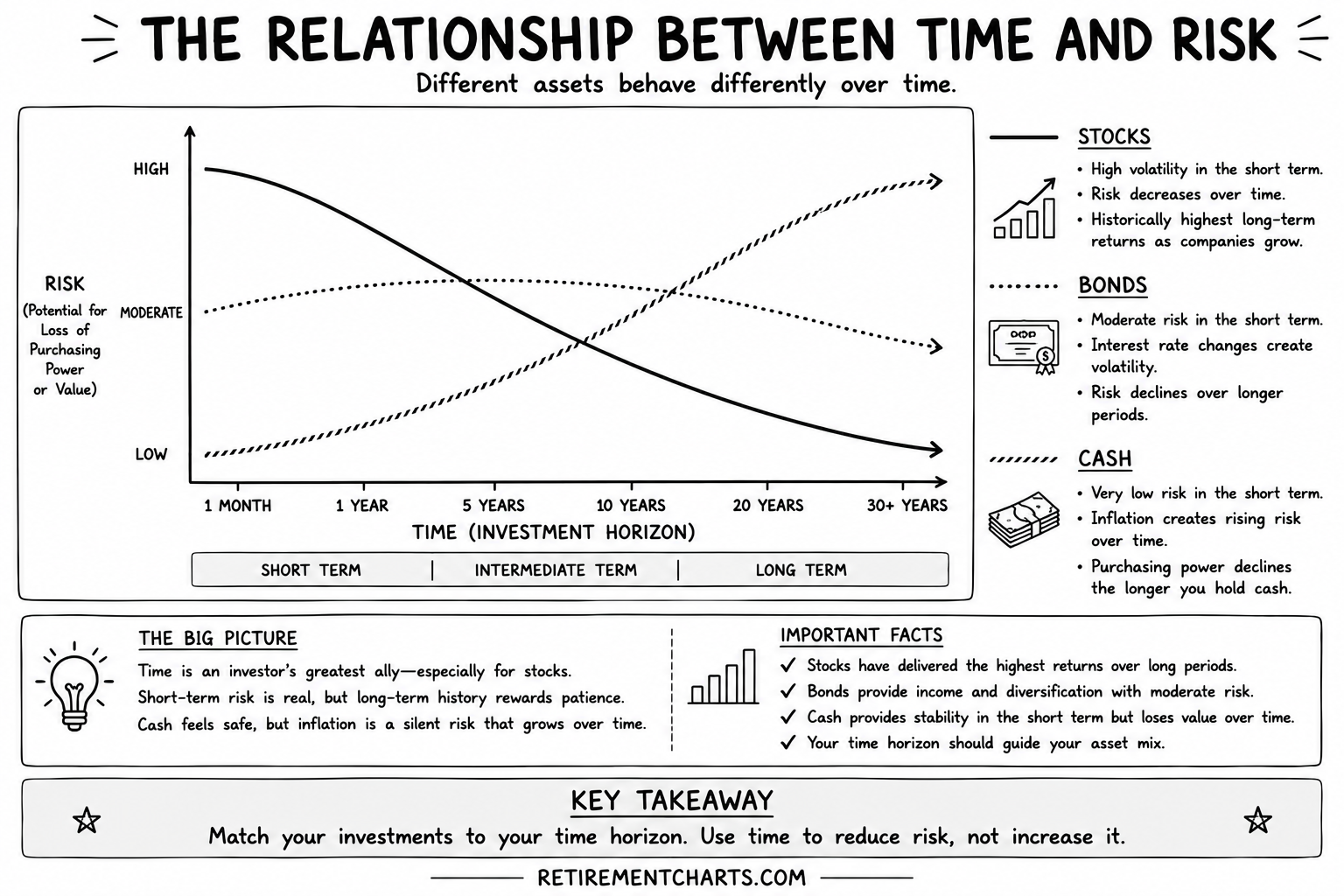

The chart above illustrates this relationship by showing how the risk characteristics of stocks, bonds, and cash evolve over time.

Understanding these relationships can help investors make better decisions, build more appropriate portfolios, and avoid costly mistakes.

Defining Risk

Before discussing the individual asset classes, it is important to define what we mean by risk.

Many investors think of risk solely as volatility. They see prices moving up and down and assume that volatility equals risk.

While volatility is certainly one form of risk, it is not the only one.

For long-term investors, risk can also mean failing to achieve financial goals, losing purchasing power to inflation, or not generating enough growth to support future spending needs.

In other words, risk is not simply about temporary declines. It is also about the possibility that your money may not do what you need it to do.

This broader definition helps explain why the relationship between time and risk can be counterintuitive.

Stocks: High Risk Today, Lower Risk Tomorrow

Stocks are often viewed as the riskiest major asset class.

That perception is understandable.

Stock prices can fluctuate dramatically over short periods. A diversified stock portfolio can decline 20%, 30%, or even 50% during severe market downturns.

For investors with short time horizons, that volatility creates substantial risk.

Imagine needing money next year for a home purchase or retirement income. A significant market decline at the wrong time could have serious consequences.

This is why the chart shows stocks carrying relatively high risk over shorter periods.

However, something interesting happens as the time horizon extends.

Over longer periods, stocks have historically rewarded patient investors with higher returns than most other asset classes. Businesses grow. Earnings increase. Dividends are paid. Economies expand.

While short-term outcomes are unpredictable, long-term outcomes have historically become more favorable.

The longer an investor remains invested, the more opportunity there is for market declines to be followed by recoveries and growth.

This is why the risk line for stocks slopes downward over time.

The short-term volatility never completely disappears, but the probability of achieving positive long-term outcomes has historically improved dramatically as holding periods increase.

For investors with horizons measured in decades rather than months, stocks often become less risky than they initially appear.

Bonds: The Middle Ground

Bonds occupy a unique position between stocks and cash.

They generally experience less volatility than stocks and have historically provided income and stability within diversified portfolios.

However, bonds are not risk-free.

Interest rates, inflation expectations, and credit conditions can all influence bond prices.

The bond market reminded investors of this reality during 2022, when rising interest rates caused many bond portfolios to experience losses that surprised investors who assumed bonds could only provide stability.

In the short term, bonds typically carry moderate risk.

They are generally less volatile than stocks but more volatile than cash.

Over longer periods, bonds have historically provided a combination of income and capital preservation that helps reduce overall portfolio risk.

Unlike stocks, however, bonds do not benefit from the same long-term growth engine created by corporate earnings and economic expansion.

As a result, bonds tend to occupy the middle ground throughout the investment horizon.

They provide diversification, income, and stability, but they may not generate enough growth to fully overcome inflation over very long periods.

For many investors, bonds serve as an important balancing force within a portfolio rather than a primary wealth-building engine.

Cash: Safe Today, Risky Tomorrow

Cash is often considered the safest investment available.

In the short term, that assessment is generally correct.

Cash does not experience stock market volatility. It does not fluctuate in value the way stocks and bonds do. It provides liquidity and stability.

If you need money next month, cash is typically one of the safest places to keep it.

This is why the chart shows cash carrying very low short-term risk.

However, cash introduces a different type of risk that becomes increasingly important over time.

That risk is inflation.

Inflation slowly erodes purchasing power. Even modest inflation rates can significantly reduce the value of money over long periods.

Consider a dollar held in cash for thirty years. While the dollar still exists, its purchasing power may be dramatically lower than when it was originally earned.

This is why the risk line for cash rises as the investment horizon increases.

Cash protects against short-term volatility but creates long-term purchasing power risk.

For investors saving for goals that are decades away, holding large amounts of cash may actually increase the probability of falling short of those goals.

In this sense, cash can become one of the riskiest long-term investments despite feeling very safe in the moment.

Matching Investments to Time Horizons

One of the most important lessons from this chart is that investment decisions should be aligned with time horizons.

Money needed in the next year should probably not be invested entirely in stocks.

Conversely, money that will not be needed for thirty years may not belong entirely in cash.

The appropriate investment depends not only on an investor's risk tolerance but also on when the money will be needed.

This concept is often overlooked.

Investors frequently focus on recent market performance rather than the timeline associated with their goals.

The result can be portfolios that are either too aggressive or too conservative.

Understanding the relationship between time and risk helps investors avoid both extremes.

The Big Picture

Time is one of the most powerful tools available to investors.

For stocks, time can reduce the impact of short-term volatility and improve the probability of positive outcomes.

For bonds, time provides income and stability while helping balance portfolio risk.

For cash, time reveals the hidden danger of inflation and lost purchasing power.

The key insight is that no asset class is universally safe or universally risky.

Every investment must be evaluated within the context of a specific time horizon and financial goal.

The Bottom Line

Many investors think about risk incorrectly.

They focus exclusively on volatility while ignoring inflation, purchasing power, and long-term growth.

The reality is that risk changes over time.

Stocks may appear risky in the short term but have historically become less risky over longer periods because of their growth potential.

Cash may appear safe in the short term but can become increasingly risky over time as inflation erodes purchasing power.

Bonds occupy the middle ground, providing income and diversification while balancing growth and stability.

Successful investing is not about avoiding risk entirely.

It is about understanding the different types of risk and matching your investments to your time horizon.

The longer your time horizon, the more important it becomes to think beyond short-term volatility and focus on the risks that matter most over the decades ahead.