The Basics of Estate Planning: Protecting the People and Causes You Care About

When most people hear the phrase estate planning, they immediately think about wealthy families, complex trusts, or large estates.

In reality, estate planning is something almost everyone needs.

Whether your net worth is $100,000 or $10 million, estate planning is ultimately about making sure the people you care about are protected and that your wishes are carried out if you become incapacitated or pass away.

A good estate plan can provide clarity during difficult times, reduce stress for family members, avoid unnecessary legal complications, and ensure that your assets end up where you intended.

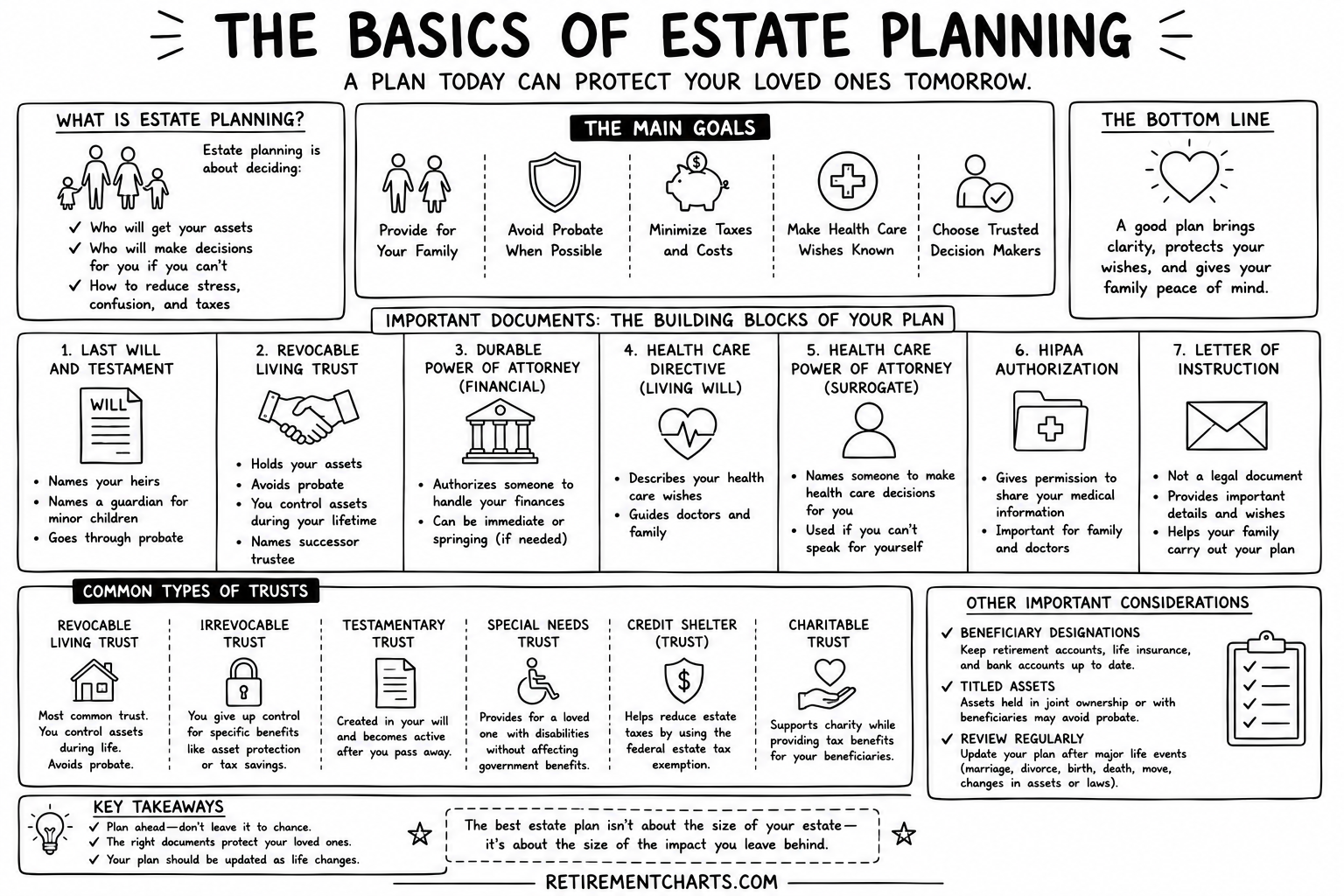

The chart above provides an overview of the major components of a comprehensive estate plan. While every situation is unique, understanding the basic building blocks can help you determine whether your own plan is complete.

What Is Estate Planning?

At its core, estate planning is the process of deciding what happens to your assets, your healthcare decisions, and your financial affairs if you are no longer able to manage them yourself.

Many people assume estate planning is only about what happens after death. In reality, a large portion of estate planning focuses on what happens during your lifetime if you become ill, injured, or mentally incapacitated.

A well-designed estate plan answers several important questions:

Who will receive your assets?

Who will manage your finances if you cannot?

Who will make healthcare decisions on your behalf?

How can your family avoid unnecessary legal complications?

How can taxes and administrative costs be minimized?

The answers to these questions are typically addressed through a collection of legal documents working together as a coordinated plan.

Last Will and Testament

The foundation of many estate plans is a Last Will and Testament.

A will outlines who receives your assets after death and names an executor who will oversee the administration of your estate.

For parents of minor children, a will is particularly important because it allows you to designate guardians.

Without a valid will, state law determines how assets are distributed and who may be responsible for managing certain aspects of your estate.

While wills are important, they generally do not avoid probate. Probate is the legal process through which a court validates the will and oversees the distribution of assets.

For some families, probate may be relatively straightforward. For others, it can be time-consuming and expensive.

This is one reason many people also utilize trusts.

Revocable Living Trust

One of the most common estate planning tools is the Revocable Living Trust.

A revocable trust allows you to transfer assets into the trust while maintaining full control during your lifetime.

You can buy, sell, invest, spend, and manage trust assets just as you normally would.

The primary advantage of a revocable trust is that assets properly titled in the trust often avoid probate upon death.

The trust also provides continuity if you become incapacitated, allowing a successor trustee to step in and manage affairs without court intervention.

For many families, a revocable trust serves as the central organizing document of an estate plan.

Durable Financial Power of Attorney

A Durable Financial Power of Attorney allows you to appoint someone to manage financial matters on your behalf.

This document can be extremely important if you become unable to handle your own finances.

The individual you appoint may be authorized to pay bills, manage accounts, handle investments, file taxes, and conduct other financial transactions.

Without this document, family members may need to seek court approval to manage your affairs, which can be costly and time-consuming.

A properly drafted power of attorney often helps families avoid significant legal complications during periods of incapacity.

Healthcare Directive

A Healthcare Directive, often referred to as a Living Will, addresses medical decisions.

This document communicates your wishes regarding medical treatment if you become unable to express those wishes yourself.

Healthcare directives may address life-sustaining treatment, artificial nutrition, resuscitation preferences, and other important healthcare decisions.

By documenting your preferences in advance, you can provide guidance to both your loved ones and medical professionals during difficult circumstances.

Healthcare Power of Attorney

In addition to a healthcare directive, many people appoint a healthcare agent through a Healthcare Power of Attorney.

This individual is authorized to make medical decisions on your behalf when you cannot do so yourself.

Selecting the right person is important.

Ideally, this individual understands your values, communicates effectively with medical professionals, and is willing to advocate for your wishes.

Together, the healthcare directive and healthcare power of attorney form the foundation of most healthcare planning.

HIPAA Authorization

Healthcare privacy laws can sometimes make it difficult for family members to obtain medical information.

A HIPAA Authorization grants permission for designated individuals to access medical records and communicate with healthcare providers.

This simple document can help avoid confusion and delays during medical emergencies.

Many estate planning attorneys consider it an essential part of a complete plan.

Letter of Instruction

Although not legally binding, a Letter of Instruction can be extremely valuable.

This document provides practical information that may not belong in formal legal documents.

Examples include:

Location of important records

Online account information

Funeral preferences

Contact information for advisors

Personal messages to family members

A letter of instruction can help loved ones navigate a difficult period with greater clarity and confidence.

Understanding Common Types of Trusts

Many people hear the word trust and assume there is only one type.

In reality, trusts can serve many different purposes.

A Revocable Living Trust is the most common trust used for probate avoidance and incapacity planning.

An Irrevocable Trust generally involves giving up some degree of control over assets in exchange for potential benefits such as creditor protection, estate tax planning, or asset protection.

A Testamentary Trust is created through a will and becomes active after death.

A Special Needs Trust can provide support for a loved one with disabilities while helping preserve eligibility for certain government benefits.

A Charitable Trust can support philanthropic goals while potentially creating tax advantages.

Historically, Credit Shelter Trusts were frequently used to help married couples reduce federal estate taxes. While estate tax exemptions are much higher today than they once were, these trusts still play a role in certain situations.

The appropriate trust structure depends on individual circumstances, goals, and family dynamics.

Beneficiary Designations Matter

One of the most common estate planning mistakes involves beneficiary designations.

Retirement accounts, life insurance policies, annuities, and many financial accounts pass directly to named beneficiaries.

These designations generally override instructions contained in a will.

As a result, it is critical to review beneficiary designations regularly.

An outdated beneficiary form can create unintended consequences and undermine an otherwise well-designed estate plan.

Estate Planning Is Not a One-Time Event

Many people create estate planning documents and never look at them again.

Unfortunately, life changes.

Marriages occur.

Children are born.

Divorces happen.

Grandchildren arrive.

Assets grow.

Tax laws evolve.

An estate plan should be reviewed periodically to ensure it still reflects your goals and circumstances.

For many families, a review every few years is a sensible approach.

The Bottom Line

The best estate plan is not necessarily the most complicated one.

It is the one that clearly communicates your wishes, protects your loved ones, and provides a framework for managing life's uncertainties.

At a minimum, most adults should consider a will, powers of attorney, healthcare documents, and updated beneficiary designations.

For many families, a revocable living trust may also be an important component.

Estate planning is ultimately an act of care.

It is not about preparing for death.

It is about making life easier for the people you love when they need it most.