Behavioral Finance: Why Your Biggest Investing Risk May Be Looking Back at You in the Mirror

Most investors believe successful investing is primarily about intelligence.

They assume the best investors are those with the highest IQs, the most advanced financial models, or the greatest ability to predict the future.

Behavioral finance tells a different story.

In many cases, the biggest determinant of investing success is not intelligence, education, or even investment selection. It is behavior.

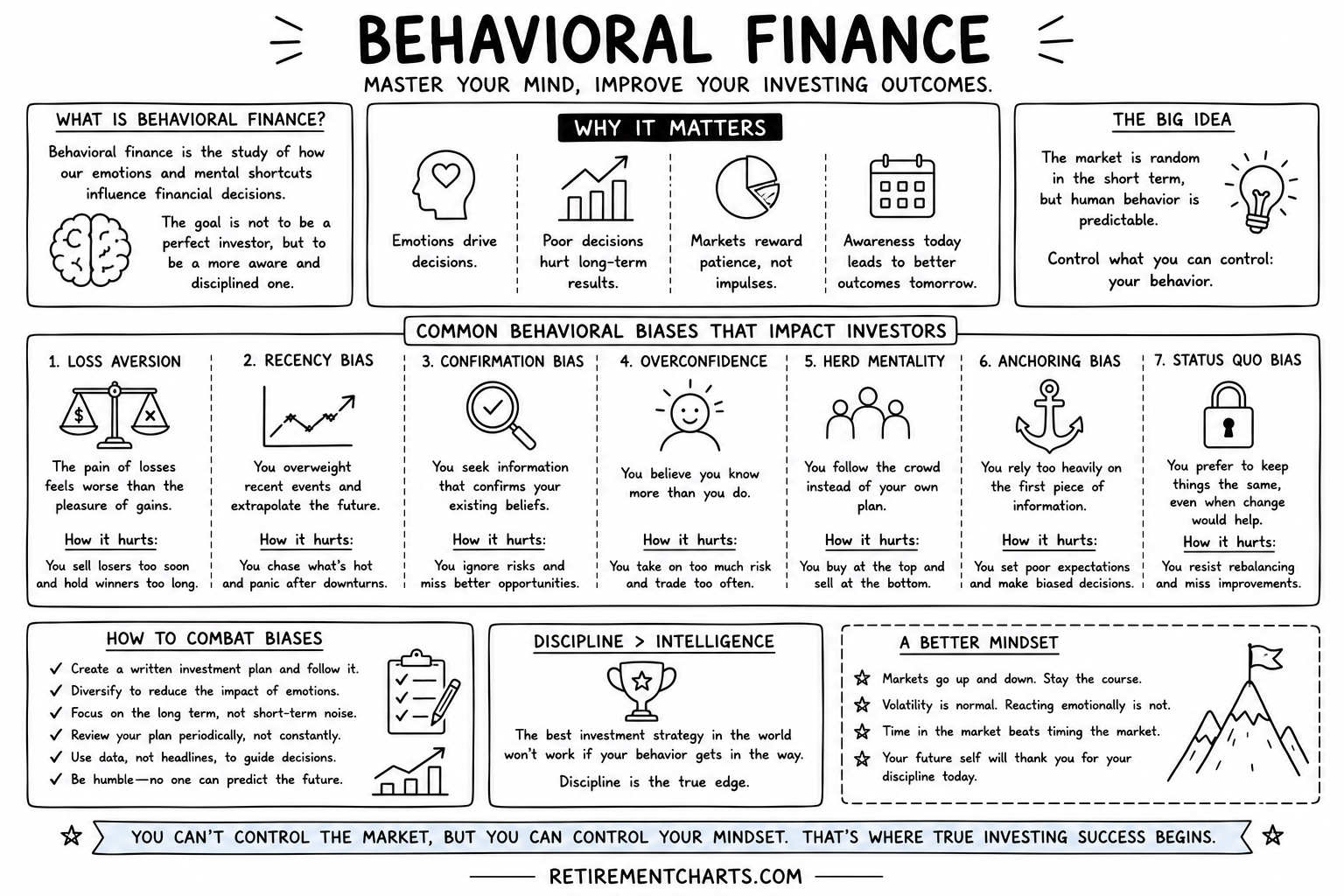

Behavioral finance is the study of how psychology influences financial decisions. It examines how emotions, mental shortcuts, biases, and human tendencies impact the choices investors make.

The field emerged as researchers began noticing that investors often behaved in ways that traditional economic theories could not explain. Rather than acting rationally at all times, people frequently make decisions based on fear, greed, overconfidence, and emotion.

Understanding behavioral finance can help investors recognize these tendencies and avoid costly mistakes.

The goal is not to become a perfect investor. The goal is to become a more aware and disciplined one.

Why Behavioral Finance Matters

Financial markets can be unpredictable in the short term.

Economic forecasts are often wrong.

Market predictions frequently miss the mark.

Yet despite all this uncertainty, one thing remains remarkably consistent: human behavior.

Investors tend to become optimistic after markets have risen and pessimistic after markets have fallen.

They chase recent winners.

They panic during downturns.

They become overconfident after success and overly fearful after losses.

Unfortunately, these emotional reactions often lead to poor financial decisions.

Many investors buy when prices are high because they feel confident and optimistic. Then they sell when prices are low because they feel scared and uncertain.

This behavior is the opposite of what creates long-term wealth.

Behavioral finance helps explain why these patterns occur and how investors can reduce their impact.

Loss Aversion

One of the most powerful concepts in behavioral finance is loss aversion.

Research suggests that the pain of losing money is often felt much more intensely than the pleasure of gaining the same amount.

For example, losing $10,000 generally feels far worse than gaining $10,000 feels good.

This emotional imbalance can create significant investing problems.

Investors may become overly conservative after experiencing losses. They may sell investments during market declines simply to stop the emotional discomfort.

The problem is that temporary market declines are a normal part of investing.

When investors allow loss aversion to drive decisions, they often lock in losses and miss future recoveries.

Recency Bias

Recency bias occurs when investors place too much weight on recent events.

If the market has been rising, people often assume it will continue rising indefinitely.

If the market has been falling, they may assume further declines are inevitable.

This tendency causes investors to extrapolate recent experiences into the future.

During bull markets, recency bias can encourage excessive optimism.

During bear markets, it can create excessive pessimism.

Neither approach is particularly helpful.

Successful investors recognize that markets move in cycles and that recent performance does not guarantee future results.

Confirmation Bias

Most people enjoy information that supports what they already believe.

Confirmation bias occurs when investors seek out information that validates existing opinions while ignoring evidence that contradicts them.

An investor who believes stocks are overpriced may only read bearish articles.

An investor who believes a particular company is a great investment may focus exclusively on positive news.

The danger is obvious.

When investors surround themselves with information that confirms their views, they may miss important risks or alternative perspectives.

Good investing often requires intellectual humility and a willingness to challenge your own assumptions.

Overconfidence

Overconfidence is one of the most common investing mistakes.

Most people believe they are above average drivers.

Most investors also believe they are above average investors.

Obviously, everyone cannot be above average.

Overconfidence can lead investors to take excessive risks, trade too frequently, or believe they possess predictive abilities they do not actually have.

Research has repeatedly shown that excessive trading often reduces long-term returns.

Investors who believe they can consistently outsmart the market frequently discover that the market is much harder to predict than they expected.

Confidence is valuable.

Overconfidence can be expensive.

Herd Mentality

Humans are social creatures.

We naturally look to others when making decisions.

While this tendency can be useful in many situations, it can create problems in investing.

Herd mentality occurs when investors follow the crowd rather than relying on a thoughtful plan.

This behavior is often visible during speculative bubbles.

As prices rise, more people become interested.

As more people buy, prices rise further.

Eventually, investors begin purchasing assets simply because everyone else appears to be doing so.

The same phenomenon can occur during market declines.

Fear spreads quickly, and investors rush to sell because others are selling.

Herd mentality often leads investors to buy high and sell low.

Anchoring Bias

Anchoring bias occurs when investors become overly attached to a specific piece of information.

For example, an investor might focus on the price they originally paid for a stock.

If the stock falls, they may refuse to sell because they are anchored to the original purchase price.

The market, however, does not care what price you paid.

Investment decisions should be based on current facts and future expectations rather than historical reference points.

Anchoring can cloud judgment and prevent rational decision-making.

Status Quo Bias

Many investors prefer doing nothing, even when change may be beneficial.

This tendency is known as status quo bias.

People often stick with outdated investment allocations, neglected retirement accounts, or inefficient strategies simply because change feels uncomfortable.

The status quo feels safe.

Unfortunately, avoiding necessary adjustments can create long-term problems.

Successful investing often requires periodic rebalancing, review, and adaptation.

Doing nothing is not always the safest choice.

How Investors Can Combat Behavioral Biases

The good news is that behavioral biases can be managed.

The first step is awareness.

Once investors recognize these tendencies, they become easier to identify.

A written investment plan can also help.

Having predetermined rules reduces the likelihood of emotional decisions during periods of market stress.

Diversification can provide another layer of protection.

A diversified portfolio helps reduce the impact of any single investment or market event.

Investors should also focus on long-term goals rather than short-term headlines.

Financial news is designed to capture attention, not necessarily improve investment outcomes.

Reviewing a portfolio periodically rather than constantly can help reduce emotional reactions to normal market fluctuations.

Finally, maintaining humility is critical.

No one consistently predicts the future.

Acknowledging uncertainty often leads to better decision-making.

Discipline Beats Intelligence

One of the most important lessons in behavioral finance is that discipline often matters more than intelligence.

A brilliant investor who constantly reacts emotionally may underperform a disciplined investor with a simple, well-constructed plan.

The best investment strategy in the world cannot help someone who abandons it during difficult times.

Long-term success comes from consistency, patience, and emotional control.

Markets will rise and fall.

News headlines will create fear and excitement.

Predictions will come and go.

Through it all, disciplined investors remain focused on the things they can control.

The Bottom Line

You cannot control the market.

You cannot control interest rates.

You cannot control economic growth or political events.

What you can control is your behavior.

Behavioral finance teaches us that investing success is often less about finding the perfect investment and more about avoiding predictable mistakes.

Loss aversion, recency bias, confirmation bias, overconfidence, herd mentality, anchoring bias, and status quo bias can all influence decisions in ways that hurt long-term returns.

The investors who achieve the best outcomes are not necessarily the smartest.

They are often the most disciplined.

Master your emotions, stay focused on your plan, and remember that your greatest investing edge may simply be avoiding the behavioral mistakes that trap so many others.